Council Constitution 09 Part 4 - Financial Procedure Rules

Contents

-

Financial Procedure Rules

- Status of Financial Procedure Rules

-

A: Financial Management

- Responsibilities of the CFO

- Responsibilities of Chief Officers

- Financial Accountabilities in relation to the Scheme of Revenue Virement (including HRA)

- Financial Accountabilities in Relation to the Treatment of Year-end Balances

- Financial Accountabilities in Relation to Accounting Policies

- Financial Accountabilities in relation to Accounting Records and Returns

- Financial Accountabilities in relation to the Annual Statement of Accounts

-

B: Financial Planning

- Responsibilities of the CFO

- Responsibilities of Chief Officers

- Format of the Budget

- Revenue Budget Preparation, Monitoring and Control

- Maintenance of Reserves and Balances

- Capital Programme Management (General Fund and Housing Revenue Account (HRA))

- Capital Programme Management Responsibilities

- Table 1 – Capital Approvals

-

C: Risk Management and Control of Resources

- Risk Management

- Internal Control

- Audit Requirements – Internal Audit

- Audit Requirements – External Audit

- Preventing Fraud and Corruption

- Assets – Security

- Asets – Disposal

- Treasury Management

-

D: Systems and Procedures

- General

- Income

- Ordering and Paying for Work, Goods and Services

- Payments to Employees and Members

- Taxation

- Quasi Commercial operations

-

E: External Arrangements

- Partnerships

- External Funding

- Work for Third Parties

-

Appendix 1 - Strategic Capital Board - Terms of Reference

- Note

- Statement of Purpose

- Attendees

- Core Functions

-

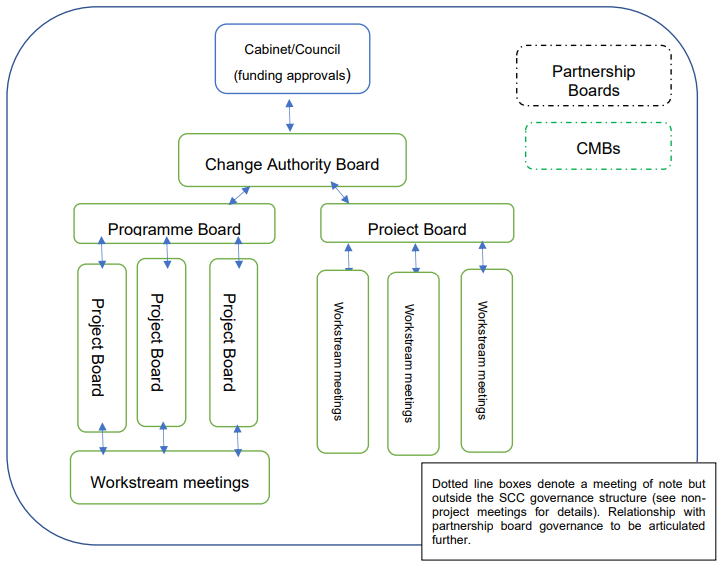

Appendix 2 - Change Authority Board

- Terms of Reference

- Project governance – key meetings

-

Appendix 3-6

- Appendix 3 _ Scheme Approval Process

- Appendix 4 - Decision Pathway for Capital Approvals

- Appendix 5 - Timeline for Capital Approvals (General Fund and HRA)

- Appendix 6 - Glossary of Terms and Acronyms

Financial Procedure Rules

Status of Financial Procedure Rules

The Financial Procedure Rules consist of and should be interpreted as the Council’s Financial Regulations

- The Council’s Financial Procedure Rules provide the framework for managing the authority’s financial affairs. They apply to every Member and Officer of the authority and anyone acting on its behalf and compliance with these rules is mandatory. These rules must be read in conjunction with the whole of the Constitution and any other Council Standards.

- The rules identify the financial responsibilities of Full Council, Cabinet, Members and Officers. Chief Officers are defined for the purpose of these rules as the Chief Executive Officer (CEO), Monitoring Officer, Chief Financial Officer (CFO) and Executive Directors. All Members and Officers have a general responsibility for taking reasonable action to provide for the security of the assets under their control, and for ensuring that the use of these resources is legal, properly authorised, provides value for money and achieves best value.

- Deliberate disregard of the Financial Procedure Rules will be seen as gross misconduct and dealt with accordingly through the disciplinary procedure.

- The CFO is responsible for maintaining a continuous review of the Financial Procedure Rules and may, where they consider it necessary, issue revisions during the year. Where the CFO considers the revisions to be significant and material additions or changes, these will be reported to Full Council for noting and/or approval. The CFO is also responsible for reporting, where appropriate, any breach of the Financial Procedure Rules to Full Council and/or to Cabinet. It should be noted that the CFO and S151 Officer is the Executive Director for Finance and Commercialisation. Any reference to CFO within these Financial Procedure Rules should be read as referring to that officer.

- To underpin the Financial Procedure Rules, the CFO is responsible for issuing any relevant advice and guidance that Members, Officers and others acting on behalf of the authority are required to follow. Such advice and guidance will be reviewed, and amended as necessary, by the CFO.

- Chief Officers are responsible for ensuring that all staff in their departments are aware of the existence and content of the authority’s Financial Procedure Rules and other internal regulatory documents and that they comply with them. An electronic copy can be found on the Council’s website.

- If it is felt to be in the wider interests of the Council, if an urgent decision is required that either:

- Falls outside of the defined process or limits within Financial Regulations or Financial Procedure Rules, or

- Is within the limits of the Financial Regulations or Financial Procedure Rules but due to reasons of urgency the rules cannot be applied as set out

A record of any authorised exceptions will be kept by the Chief Internal Auditor to assist the S151 Officer in determining if any amendments need to be made to these rules.

A: Financial Management

Responsibilities of the CFO

- A.1 To ensure the proper administration of the financial affairs of the authority.

- A.2 To monitor compliance with the Financial Procedure Rules.

- A.3 To ensure proper professional practices are adhered to and to act as head of profession in relation to the standards, performance and development of finance staff throughout the authority.

- A.4 To advise on the key strategic controls necessary to secure sound financial management.

- A.5 To ensure that financial information is available to enable accurate and timely monitoring and reporting of comparisons of national and local financial performance indicators.

Responsibilities of Chief Officers

- A.6 To ensure that all staff in their area are aware of the Financial Procedure Rules in their departments and to monitor adherence

to the standards and practices, liaising as necessary with the CFO. - A.7 To ensure there are sound financial practices in relation to the standards, performance and

development of staff in their departments.

Financial Accountabilities in relation to the Scheme of Revenue Virement (including HRA)

Explanatory Note

The overall budget is agreed by Cabinet and approved by Full Council. Following this approval Chief Officers and budget holders are authorised to incur net expenditure in accordance with the estimates that make up the budget for the current financial year. The rules below cover virements, or the switching of resources between approved estimates, heads of expenditure and income.

What is a Virement?

A virement is the: ‘planned transfer of a budget for use in a different purpose to that originally intended’.

A virement does not create additional overall budget liability. It changes the purpose for which the budget will be used compared to that originally planned. The use of virements is intended to enable services to manage budgets with a degree of flexibility while at the same time ensuring that these remain consistent with the overall policy framework determined by the Council.

Chief Officers are expected to exercise their discretion in managing their budgets responsibly and prudently, within any agreed restrictions on spending. They should avoid supporting recurring expenditure from virements against one-off sources of savings or additional income, or creating future commitments, including full-year effects of decisions made part way through a year, for which they have not identified future resources.

Chief Officers must plan to fund such commitments from within their own budgets having regard to the overall forecast outturn for the service, and the Council. Any budget provided by Full Council to meet specific pressures must be used for the identified purpose. If this budget subsequently is not required, this should be identified to the CFO to enable the resource to be utilised as he/she sees fit.

Executive Directors should balance their service area net expenditure to the budget allocated. In some cases, this will require a transfer of the budget between their service activities.

For the purposes of the scheme set out below, a virement occurs when a budget is transferred from one Service Activity to another. Service activities that will apply for the following financial year are those which are set out in the budget approved by Full Council for the coming financial year.

- A.8 All virements should be cleared in the first instance by the relevant accounting support for the Service Activity concerned. All virements must be recorded on the ledger system.

- A.9 Controls on the use of additional controllable income are required to ensure that significant additional income is not spent without any control process in place.

- A.10 Decisions will be made in line with the criteria set out in the table below and applies to virements of expenditure budgets or virements of income budgets:

| Virement Value | Approval Required |

|---|---|

| Up to £20,000 | Approved by CHIEF OFFICERS in consultation with the CFO |

| £200,000 to £500,000 | Approved by CHIEF OFFICERS in consultation with CFO and Cabinet Member |

| Over £500,000 to £2 million | Approved by CABINET |

| Over £2 million | Approved by COUNCIL |

- A.11 The creation of any new reserve, or change in use of reserve, needs agreement from the CFO and formal approval by Cabinet. The CFO can allocate sums of any value to or from central funds or reserves, in line with the requirements for virements as outlined in the above table.

- A.12 Any budget virements resulting from a restructure or a reduction in the number of FTE can only be actioned following the appropriate consultation.

- A.13 The HRA contingency and revenue balance is defined as a “non-employee” budget. However, any virements from the HRA revenue balance that would reduce the level of balances below the minimum level set by the CFO in the HRA budget and business plan report can only be approved by Full Council.

Financial Accountabilities in Relation to the Treatment of Year-end Balances

Responsibilities of the CFO

- A.14 Where the council is in an underspend position the CFO is responsible for administering the scheme of carry-forward within the guidelines approved by Full Council. If the council is in an overspend position only carry forwards that relate to grant income will be considered

- A.15 To report all underspends on service estimates carried forward to Full Council for

approval.

Responsibilities of Chief Officers

- A.16 Any overspends will be reported by the CFO to Cabinet and to Full Council.

09 Part 4 - Financial Procedure Rules - 6 - May 2022 - A.17 There is no authority to overspend. Budgets are allocated on a ‘cash limit’ basis. This means the service must operate within the agreed set budget. If a budget is forecast to overspend, this must be offset by mitigation measures or an underspend elsewhere to ensure the cash limit is not breached. The Executive Director will be responsible for bringing forward, at the earliest opportunity, a plan of mitigation that will result in the overspend being contained within budget. Such a plan will be expected to be sufficiently detailed, with timeframes, milestones, performance indicators and any resources needed, that it is considered a robust plan by the Executive Director Corporate Services. Where, in spite of this, a Chief Officer believes they may overspend

they must inform the CFO immediately. - A.18 Executive Directors will be requested to sign a declaration before the commencement of the financial year, stating they understand the cash limited budget set and the key assumptions and any savings it includes, and they will make every effort to stay within that limit. Budget holders will be requested to agree the budgets under their management and sign an accountability statement stating that they understand their role as a budget holder and the support they will receive in managing their financial position.

- A.19 Underspends on specific estimates may be carried forward within guidelines issued by the

CFO, subject to the approval of Full Council. However, where budgets being carried

forward into the new financial year are ring-fenced (e.g. specific grant funds from

Government) and hence the Council can exercise no discretion, these will not require the

approval of Full Council. - A.20 Schools’ balances shall be available for carry-forward to support the expenditure of the

school concerned as per the criteria in surplus policy. Schools cannot plan for a year end

deficit budget when submitting budget plans at the start of the year. Schools that submit

deficit plans will be required to resubmit their budget with plans to bring the budget back

into balance. The authority will intervene if a school refuses to set a balanced budget by

identifying the action a school could take and ultimately by suspending delegation. - A.21 Where an unplanned deficit occurs, the governing body shall prepare a detailed financial

recovery plan for consideration by the Cabinet Member concerned and agreed by Cabinet, following evaluation

by the relevant Chief Officer and the CFO. Any unplanned deficit incurred during the year

would be a first call on the following year’s budget; the school would need to include the

deficit in its balanced budget plan for the following year. Schools that incur unplanned

deficits in successive years would be treated the same as schools submitting deficit plans

and the authority would need to intervene. The school will need to work with SCC’s School

Finance Team (if they have purchased SCC Finance Services via an SLA) or their own

finance support (if they have not bought back SCC Finance Services), together with SCC

School Improvement Teams to produce a robust Deficit Recovery Plan (DRP), ensuring

the spend is brought back in line with their allocated funds. - A.22 The schools funding comes from Dedicated Schools Grant (DSG) grant. DSG consists of

three blocks namely Schools Block, Early Years Block and High Needs Block. The grant

is paid in support of the local authority’s schools budget. Local authorities are responsible

for determining the split of the grant between central expenditure and the individual

schools budget (ISB) in conjunction with local schools forums. Local authorities are

responsible for allocating the ISB to individual schools in accordance with the local

schools’ funding formula - A.23 Scheme for financing schools sets out the financial relationship between the City Council

and the maintained schools it funds. The scheme for financing schools is required by the

School Standards and Framework Act 1998 and it contains requirements relating to

financial management and associated issues. The scheme is binding on both the local

authority and schools.

The scheme refers to the following legislation:

Financial Accountabilities in Relation to Accounting Policies

Responsibilities of the CFO

- A.24 To select suitable accounting policies, and to ensure that they are applied consistently.

The accounting policies are set out in the Statement of Accounts, which are prepared at

31 March each year, and covers such items as:- a) General principles

- b) Adjustments between accounting basis and funding basis

- c) Acquisitions and discontinued operations

- d) Cash and cash equivalents

- e) Exceptional items

- f) Prior period adjustments, changes in accounting policies and estimates and

errors - g) Employee benefits

- h) Events after the balance sheet date

- i) Financial Instruments

- j) Government grants and other contributions

- k) Heritage assets

- l) Interests in companies and other entities

- m) Investment property

- n) Joint arrangements

- o) Leases

- p) Overhead and support services

- q) Property, Plant and Equipment (PPE)

- r) Private Finance Initiatives (PFI) and similar contract

- s) Provision, contingent liabilities and contingent assets

- t) Reserves

- u) Revenue expenditure funded from capital under statute (REFCUS)

- v) Value added tax (VAT)

- w) Collection fund

- x) Schools

- y) Rounding convention

Responsibilities of Chief Officers

- A.25 To adhere to the accounting policies and guidelines approved by the CFO

Financial Accountabilities in relation to Accounting Records and Returns

- A.26 To determine the accounting procedures and records for the authority. Where these are maintained outside the finance department, the Chief Officer concerned should consult the CFO.

- A.27 To arrange for the compilation of all accounts and accounting records under his or her direction.

- A.28 To comply with the following principles when allocating accounting duties:

- a) Separating the duties of providing information about sums due to or from the authority and calculating, checking and recording these sums from the duty of collecting or disbursing them

- (b) Employees with the duty of examining or checking the accounts of cash transactions must not themselves be engaged in these transactions.

- A.29 To make proper arrangements for the audit of the authority’s accounts in accordance with the Accounts and Audit Regulations 2015.

- A.30 To ensure that all claims for funds including grants are made by the due date.

- A.31 To prepare and publish the draft accounts of the authority for each financial year, in accordance with the statutory timetable, which is 31 May other than for financial years 2020/21 and 2021/22 when it is 31 July. With the requirement for the Governance Committee to approve the audited statement of accounts and for them to be published by 31 July other than for financial years 2020/21 and 2021/22 when it is 30 September.

- A.32 To administer the authority’s arrangements for underspends or overspends to be carried forward to the following financial year.

- A.33 To ensure the proper retention of financial documents in accordance with the requirements set out in the authority’s document retention schedule.

Responsibilities of Chief Officers

- A.34 To consult and obtain the approval of the CFO before making any changes to accounting records and procedures.

- A.35 To comply with the principles outlined in paragraph A.27, when allocating accounting duties.

- A.36 To maintain adequate records to provide an audit trail leading from the source of income/expenditure through to the accounting statements.

- A.37 To supply information required to enable the Statement of Accounts to be completed in accordance with guidelines and timetable issued by the CFO.

Financial Accountabilities in relation to the Annual Statement of Accounts

Responsibilities of the CFO

- A.38 To select suitable accounting policies and to apply them consistently.

- A.39 To make judgments and estimates that are reasonable and prudent.

- A.40 To comply with the Code of Practice on Local Authority Accounting in the United Kingdom (Code of Practice).

- A.41 To sign and date the Statement of Accounts, stating that they present a true and fair view of the financial position of the authority at the accounting date and its income and expenditure for the year ended 31 March.

- A.42 To draw up the timetable for final accounts preparation and to advise staff and external auditors accordingly.

Responsibilities of Chief Officers

- A.43 To comply with accounting guidance provided by the CFO and to supply the CFO with information when required.

B: Financial Planning

Responsibilities of the CFO

- B.1 For the General Fund, to ensure that a five-year overview is prepared on a regular basis for consideration and recommendation by Cabinet, before submission to Full Council. The CFO will also prepare the indicators required as part of the Prudential Code. Full Council may amend the budget and Prudential Indicators or ask Cabinet to reconsider them before approving them.

- B.2 For the HRA, to ensure that a 40-year business plan is produced which covers revenue and capital spending. With regard to the revenue budget, there must be a detailed budgetfor the forthcoming financial year for consideration and recommendation by Cabinet,before submission to Full Council. The CFO will also prepare the indicators required aspart of the Prudential Code. Full Council may amend the budget and Prudential Indicators or ask Cabinet to reconsider them before approving them. The 40-year business plan should also be presented to Cabinet and Full Council as part of the budget report.

- B.3 To advise and supply the financial information that needs to be included in business plans in accordance with statutory requirements and agreed timetables.

- B.4 To contribute to the development of business and service plans.

- B.5 To maintain a 5-year Medium Term Financial Strategy (MTFS) and model.

- B.6 To advise Cabinet and opposition groups on the format and content of the budget that is to be approved by Full Council. This includes providing a commentary on the robustness of the estimates made for the purpose of the calculations (to set the Council Tax), and the adequacy of the proposed level of reserves, as required by Section 25 of the Local Government Act 2003.

- B.7 Work with other Chief Officers to ensure horizon scanning and planning within the current economic climate.

Responsibilities of Chief Officers

- B.8 To ensure that systems are in place to measure activity and collect accurate information for use as performance indicators.

- B.9 To ensure that performance information is monitored sufficiently frequently to allow corrective action to be taken if targets are not likely to be met.

- B.10 To contribute to the development of performance plans in line with statutory requirements/

- B.11 To contribute to the development of corporate and service targets and objectives and performance information.

Format of the Budget

Responsibilities of the CFO

- B.12 To include a statement on the robustness of the estimates and the adequacy of the

reserve

Responsibilities of Chief Officers

- B.13 To ensure robust and up-to-date business plans are in place, together with delivery plans for any agreed savings proposals

Revenue Budget Preparation, Monitoring and Control

Responsibilities of the CFO

- B.14 To ensure sound financial administration and produce a balanced budget; as set out in S.151 of the Local Government Act 1972.

- B.15 To administer procedures to set Council Tax and Business Rates.

- B.16 To establish an appropriate framework of budgetary management and control that ensures:

- a. Expenditure is within budget unless Full Council agrees otherwise.

- b. Each Chief Officer has available timely information on receipts and payments on each budget which is sufficiently detailed to enable managers to fulfil their financial responsibilities.

- c. Expenditure is committed only against an approved budget head and within resources available.

- d. All managers responsible for committing expenditure comply with relevant guidance, and the Financial Procedure Rules.

- e. Each cost centre has a single named manager, determined by the relevant Chief Officer. As a general principle, budget responsibility should be aligned as closely as possible to the decision-making processes that commits expenditure.

- f. Significant variances from approved budgets are investigated and reported by budget managers regularly along with action plans for recovery.

- B.17 To administer the authority’s scheme of revenue virement.

- B.18 To submit reports to Cabinet and if necessary, to Full Council, following consultation with the relevant Chief Officer, where a Chief Officer is unable to balance expenditure and resources within existing approved budgets under his or her control.

- B.19 To prepare and submit reports to Cabinet on the authority’s projected income and expenditure compared with the budget on a regular basis.

- B.20 All estimates should be calculated using the approved assumptions in the MTFS.

Responsibilities of Chief Officers

- B.21 To ensure that budget estimates reflecting agreed priorities and business plans are produced in consultation with Cabinet Member and submitted to the CFO in accordance with the budget timetable and the guidance issued for the production of budget reports to Cabinet and Full Council.

- B.22 To maintain budgetary control within their departments, in adherence to the principles in B.15, and to ensure that all income and expenditure are properly recorded and accounted for.

- B.23 To ensure that an accountable budget holder is identified for each item of income and expenditure under the control of the Chief Officer (grouped together in a series of cost centres). As a general principle, budget responsibility should be aligned as closely as possible to the decision-making that commits expenditure.

- B.24 To ensure that spending remains within the service’s overall budget and that individual budget heads are not overspent, by monitoring the budget and taking appropriate corrective action where significant variations from the approved budget are forecast.

- B.25 To ensure that a monitoring process is in place to review performance levels/levels of service in conjunction with the budget, and that this process is operating effectively.

- B.26 To prepare, following consultation with the CFO, reports on the service’s projected expenditure compared with its budget, in accordance with the Council’s Corporate Monitoring procedure and timetable.

- B.27 To ensure prior approval by Full Council or Cabinet (as appropriate) for new proposals, of whatever amount, that:

- a. Create financial commitments in future years

- b. Change existing policies, initiate new policies or cease existing policies

- c. Materially extend or reduce the authority’s services

- B.28 The report on new proposals should explain the full financial implications, after consultation with the CFO. Unless Full Council or Cabinet has agreed otherwise, Chief Officers must plan to contain the financial implications of such proposals within their budget.

- B.29 To ensure compliance with the scheme of virement.

- B.30 To agree with the relevant Chief Officer and the CFO where it appears that a budget proposal, including a virement proposal, may impact materially on another service area or Chief Officer’s level of service activity.

Maintenance of Reserves and Balances

Responsibilities of the CFO

- B.30 To advise the Cabinet and Council on prudent levels of reserves and balances for the City Council, giving consideration to level of risk the council faces, and published CIPFA guidance

Capital Programme Management (General Fund and Housing Revenue Account (HRA))

Capital Governance - Capital Approvals

- B.31 The Council has an established governance process which ensures transparency and gives assurance to members. The Change Authority Board and the Strategic Capital Board will receive and consider proposals and business cases in line with the agreed

procedure and timeline for capital approvals as issued by the CFO. Further details of the role of the Change Authority Board and Strategic Capital Board are included in appendices 1 and 2. - B.32 All new capital schemes or additions to existing capital schemes would normally have a business justification through a business case to the Strategic Capital Board. These are considered for prioritisation ahead of recommendation to the Council for approval of the capital programme as part of the annual budget approval in February. Business cases for new or additional capital funding made at any other time during the year will be considered in exceptional circumstances only, unless external funding has been identified for scheme. There is a separate procedure for the HRA, as per B.33.

- B.33 Individual business cases are also normally expected for new additions to the HRA capital programme. The 40-year HRA business plan, which is approved by Full Council annually, will show the affordability of the overall programme. Capital Business cases must always consider the revenue implications of the capital spending.

- B.34 Approval is also required before expenditure can be incurred against a new scheme in the capital programme. This approval can be requested when the scheme is submitted for addition to the General Fund capital programme. If a scheme is included in the programme, but is dependent on subsequent agreement to spend, approval to spend must be sought usually once a full business case is available and prior to incurring expenditure. Approval for HRA additions and approval to spend will be given to schemes included in the 40-year HRA business plan.

- B.35 The Capital programme will operate within the limits set within the Capital Strategy, applying the agreed limits from the indicators adopted from the Prudential Code. These are designed to ensure capital spending is affordable and sustainable.

- B.36 Schemes already added to the capital programme may spend up to ten per cent of the scheme budget with the approval of the relevant Chief Officer following consultation with the relevant Cabinet Member and the CFO in advance of approval to spend on the scheme. Such cases should be based on an urgent need to spend, rather be seen as an alternative to seeking formal permission to spend by the usual means of reporting to Cabinet or Council as necessary

- B.37 The same process for considering and approving projects and business cases applies whether the decision is for an officer or a Cabinet Member. A model for business cases

is used which is streamlined for less complex projects to ensure the input is proportionate.

The full scheme approval process is detailed in Appendix 3. - B.38 The capital programme shall be recommended for approval by Full Council following consideration by the Strategic Capital Board. This will include projected available resources, the allocation of resource to schemes, the impact on the revenue budget,

prudent retention of resources to meet unforeseen short-term demands, variances in projected available resources and medium-term future needs. - B.39 In addition to the large schemes and development projects that make up much of the capital programme, there will be routine investment plans for the core business of the Council that have block allocations. These include the schools’ maintenance programme, the heritage assets maintenance budget, highways maintenance, the replacement of vehicles and other essential service assets. These are planned and budgeted for through 5-year asset management plans within the capital programme and will operate within the approved control totals. The Executive Director is delegated to move budgets between

projects within each programme. - B.40 A virement is the movement of a budget to another purpose other than that it was allocated to when the capital scheme was approved. This applies to the virement of budgets between capital schemes within the capital programme and between projects within a capital scheme.

- B.41 All virements at any value within a capital programme can be approved by the CFO on submission of a completed DDN. All other virements must be agreed according to the approval levels as set out in Table 1.

- B.42 Requests for approval by Cabinet or Council must be submitted in the correct corporate report format and submitted in accordance with Council’s democratic processes.

- B.43 Decisions will be made in line with the approval levels set out in Table 1.

Notes: A diagram summarising the process for approving new capital schemes and additions to existing capital schemes is shown in Appendix 4.

A timeline for capital approvals is shown in Appendix 5.

Capital Governance - Capital Monitoring

- B.44 The monitoring of the capital programme is part of the core business of Cabinet Member Briefing on a quarterly basis with formal decisions published in accordance with constitutional arrangements. The Strategic Capital Board has the same quarterly programme review.

- B.45 Approvals of slippage and rephasing and the approval of Delegated Decision Notices (DDNs) required to vire budgets between schemes and projects within schemes should be requested in accordance with approval levels set out in Table 1.

- B.46 Capital schemes must be monitored at a service level according to the capital monitoring timetable. This includes a review of expenditure, plans for slippage and rephasing and explanations for any variance to budget.

- B.47 Expenditure included in the Capital Programme must show the total value of contracts and related expenses that the council will incur. Any grants or other income must be shown as a source of capital finance and not as a reduction to the gross expenditure.

- B.48 Expenditure must be in line with the Council’s Contract Procedure Rules.

- B.49 Feasibility work carried out prior to a scheme being added to the capital programme is a charge to revenue. If a capital project is approved following feasibility work, the cost of this can be capitalised. Feasibility work is an analysis of all factors of the project including economic, technical, legal and scheduling considerations, to establish the likelihood that the project can be completed successfully.

Capital Programme Management Responsibilities

Local authorities are required by regulation to have regard to the Prudential Code for Capital

Finance in Local Authorities when carrying out financial duties regarding capital expenditure. The

objectives of this code are to ensure that the capital investment plans of local authorities are

affordable, prudent and sustainable. The responsibilities are set out below to ensure adherence

with this code.

Responsibilities of the CFO

- B.50 To issue guidance concerning capital schemes and controls, and to determine the

definition of “capital”, having regard to government regulations and accounting

requirements. - B.51 To ensure that the Capital Strategy and 5-year programme are presented to Full Council

as part of the budget and at such other times as the CFO may determine. The HRA capital

spending plan is included and detailed in the Council Capital report that is reported to Full

Council as part of budget-setting. - B.52 To report on the outturn of capital expenditure to Council as soon as practicable after the

end of the financial year. - B.53 To give regular updates to Cabinet on the forecast expenditure.

Responsibilities of the Strategic Capital Board

- B.54 To oversee and coordinate the preparation, review and implementation of the Council’s

Capital Strategy. The Capital Strategy must be approved by Council and reviewed

annually - B.55 To lead the strategic direction of capital investment for the Council.

- B.56 The full terms of reference for the Strategic Capital Board are attached at Appendix 1. In

summary the Strategic Capital Board will be responsible for:- a. Managing un-ringfenced and corporate resources and reviewing all bids for

resources, evaluating them and then agreeing on the prioritisation of resources

accordingly. - b. Reviewing the use of any ringfenced resources to ensure alignment with other

spending plans and the maximisation of benefits to the Council and achievement

of Council outcomes. - c. Recommending the use of both un-ringfenced and ringfenced resources and also

the general prioritisation of resources so that Cabinet / Council can make a final

well-informed decision on the utilisation of resources. - d. Prior to the annual review of the capital strategy undertaking a review of the

individual projects.

- a. Managing un-ringfenced and corporate resources and reviewing all bids for

Responsibilities of Chief Officers

- B.57 To ensure that the correct business case template is completed in full for all new capital projects. This will include full costings, accurate phasing of annual budgets across the life of the project and correctly identifying capital and revenue expenditure required for the project. The completion of the business case should be in consultation with the Finance Business Partner for the service to ensure the accuracy of the financial information provided.

- B.58 The cost of internal resources should be included in the project costs. This will include:

- Project Management

- Legal Services

- HR

- Communications

- Procurement

- Finance

Table 1 – Capital Approvals

Note: The appropriate report should be submitted for decision depending on the value of approval as per sections B41 and B42.

| Approval to add new schemes or to increase existing capital schemes Funded from new, sources including 100% ringfenced | Approval to spend against a new or existing scheme If a full business case is available, approval to spend can be given at the same time as approval to add a scheme to the capital programme or increase the value of an existing capital scheme | Virements ** Variations across schemes within an overall programme can be approved by CHIEF OFFICER*** in consultation with CFO and relevant Cabinet Member | Slippage & Rephasing Movement of budgets between years |

|---|---|---|---|

| Up to £500,000 – A Delegated Decision Notice (DDN) is required Approved by CHIEF OFFICER*** in consultation with CFO and Cabinet Member |

Up to £500,000 – A Delegated Decision Notice (DDN) is required Approved by CHIEF OFFICER*** in consultation with CFO and Cabinet Member |

Up to £500,000 – A Delegated Decision Notice (DDN) is required Approved by CHIEF OFFICER*** in consultation with CFO and Cabinet Membe |

Up to £500,000 – A Delegated Decision Notice (DDN) is required Approved by CHIEF OFFICER*** in consultation with the CFO and Cabinet Member |

| Over £500,000 up to £5 million Approved by CABINET |

Over £500,000 up to £5 million Approved by CABINET |

Over £500,000 up to £5 million Approved by CABINET |

Over £500,000 Approved by CABINET |

| Over £5 million Approved by COUNCIL |

Over £5 million Approved by COUNCIL |

Over £5 million Approved by COUNCIL |

* This includes credit arrangements such as financing leases.

** If the virement is not in line with current approved council policies and strategies the decision must be made by Council regardless of value.

***The Chief Officer is the Executive Director of the service that holds the budget for the capital project.

Following the submission of a Delegated Decision Notice (DDN) for consideration and recommendation by the Strategic Capital Board, the CFO, can approve virements of any value within a programme.

The approval limits do not apply in respect of decisions taken at the Joint Commissioning Board up to a value of £2 million where the decision is taken by an officer / Individual Cabinet Member following consultation with and the agreement of all Cabinet Member Representatives on the Board or to acquisitions and disposals in relation to the Property Investment Fund, authority being delegated to the Associate Director: Capital Assets, following consultation with the Leader of the Council and the Executive Director: Finance and Commercialisation.

C: Risk Management and Control of Resources

Risk Management

Responsibilities of the CFO

- C.1 To prepare and promote the authority’s risk management policy.

- C.2 To develop risk management controls in conjunction with other Chief Officers.

- C.3 To include all appropriate employees of the authority in a suitable fidelity guarantee insurance.

- C.4 To offer insurance cover to schools.

- C.5 To advise Cabinet on proper insurance cover where appropriate, and effect corporate insurance cover, through external insurance and internal funding.

Responsibilities of Chief Officers

- C.6 To notify the CFO immediately of any loss, liability or damage that may lead to a claim against the authority, together with any information or explanation required by the CFO or the authority’s insurers.

- C.7 To take responsibility for the management of operational and service risks in accordance with the risk management policy, having regard to advice from the CFO and other

specialist Officers. - C.8 To ensure that there are regular reviews of risk within their departments and that appropriate actions are take or are in place to manage risk.

- C.9 To notify the CFO promptly of all new risks, including properties or vehicles that require insurance and of any alterations or new initiatives affecting existing insurances.

- C.10 To consult the CFO and where appropriate the Director of Legal & Business Services, on the terms of any indemnity that the authority is requested to give.

- C.11 To ensure that employees, or anyone covered by the authority’s insurances, do not admit liability or make any offer to pay compensation that may prejudice the assessment of liability in respect of any insurance claim.

Internal Control

Responsibilities of the CFO

- C.12 To assist the authority to put in place an appropriate control environment and effective internal controls which provide reasonable assurance of effective and efficient operations, financial stewardship, probity and compliance with laws and regulations.

Responsibilities of Chief Officers

- C.13 To manage processes to check that established controls are being adhered to and to evaluate their effectiveness, in order to be confident in the proper use of resources, achievement of objectives and financial performance targets, and management of risks.

- C.14 To review existing controls in the light of changes affecting the authority and to establish and implement new ones in line with guidance from the CFO. Chief Officers should also be responsible for removing controls that are unnecessary or not cost or risk effective, for example because of duplication.

- C.15 To ensure staff have a clear understanding of the consequences of lack of control.

Audit Requirements – Internal Audit

Responsibilities of the CFO

- C.16 To ensure that internal auditors have the authority to:

- a. Access authority premises at reasonable times

- b. Access all assets, records, documents, correspondence and control systems

- c. Receive any information and explanation considered necessary concerning any matter under consideration

- d. Require any employee of the authority to account for cash, stores or any other

authority asset under his or her control - e. Access records belonging to third parties, such as contractors, when required

- f. Directly access the Head of Paid Service, Cabinet and Overview and Scrutiny

Management Committee

- C.17 To approve the strategic and annual audit plans prepared by the Chief Internal Auditor, which take account of the characteristics and relative risks of the activities involved.

- C.18 To ensure that effective procedures are in place to investigate promptly any suspected

fraud or irregularity.

Responsibilities of Chief Officers

- C.19 To ensure that internal auditors are given access at all reasonable times to premises, personnel, documents and assets that the auditors consider necessary for the purposes of their work.

- C.20 To ensure that auditors are provided with any information and explanations that they seek in the course of their work.

- C.21 To consider and respond promptly to recommendations in audit reports.

- C.22 To ensure that any agreed actions arising from audit recommendations are carried out in a timely and efficient fashion.

- C.23 To notify the CFO immediately of any suspected fraud, theft, irregularity, improper use or misappropriation of the authority’s property or resources. Pending investigation and reporting, the Chief Officer should take all necessary steps to prevent further loss and to secure records and documentation against removal or alteration.

- C.24 To ensure new systems for maintaining financial records, or records of assets, or changes to such systems, are discussed with and agreed by the Chief Internal Auditor prior to implementation.

Audit Requirements – External Audit

Responsibilities of the CFO

- C.25 To ensure that external auditors are given access at all reasonable times to premises, personnel, documents and assets that the external auditors consider necessary for the

purposes of their work. - C.26 To ensure there is effective liaison between external and internal audit.

- C.27 To work with the external auditor and advise Full Council, Cabinet and Chief Officers on their responsibilities in relation to external audit.

Responsibilities of Chief Officers

- C.28 To ensure that external auditors are given access at all reasonable times to premises, personnel, documents and assets which the external auditors consider necessary for the purposes of their work.

- C.29 To ensure that all records and systems are up to date and available for inspection.

Preventing Fraud and Corruption

Responsibilities of the CFO

- C.30 To develop and maintain an anti-fraud, anti-bribery and anti-corruption policy.

- C.31 To develop and maintain an anti-money laundering policy.

- C.32 To maintain adequate and effective internal control arrangements.

- C.33 To ensure that all suspected irregularities are reported to the Chief Internal Auditor.

Responsibilities of Chief Officers

- C.34 To ensure that all suspected irregularities are reported to the Chief Internal Auditor.

- C.35 To invoke the authority’s disciplinary procedures where the outcome of an investigation indicates improper behaviour.

- C.36 To ensure that where financial impropriety is discovered, the CFO is informed, and where sufficient evidence exists to believe that a criminal offence may have been committed, the police are called in to determine with the Crown Prosecution Service whether any prosecution will take place.

- C.37 To maintain a departmental register of interests.

Assets – Security

Responsibilities of the CFO

- C.38 To ensure that an asset register is maintained in accordance with good practice for all fixed assets whose value is material in the manner prescribed by CIPFA in the Institute's Practical Guide to Asset Registers. The function of the asset register is to provide theauthority with information about fixed assets so that they are safeguarded, used efficiently and effectively, and are adequately maintained.

- C.39 To receive the information required for accounting, costing and financial records from each Chief Officer.

- C.40 To ensure that assets are valued in accordance with the Code of Practice.

Responsibilities of Chief Officers

- C.41 The Service Manager – Asset Management shall maintain a property database in a form approved by the CFO for all land and buildings and plant within buildings currently owned or used by the authority. Any use of property by a department or establishment other than for direct service delivery should be supported by documentation identifying terms, responsibilities and duration of use.

- C.42 To ensure that lessees and other prospective occupiers of Council land are not allowed to take possession or enter the land until a lease or agreement, in a form approved by the appropriate Chief Officers has been established.

- C.43 To ensure the proper security of all buildings and other assets under their control.

- C.44 Where land or buildings are surplus to requirements, a recommendation for sale should be the subject of a joint report by the appropriate Chief Officers

- C.45 To pass title deeds to the Director of Legal & Business Services who is responsible for custody of all title deeds.

- C.46 To ensure that no authority asset is subject to personal use by an employee without proper authority.

- C.47 To ensure the safe custody of vehicles, equipment, furniture, stock, stores and other property belonging to the authority. If an asset requires to be moved, altered, or disposed of check that the asset has not been leased or that any lease conditions are complied with.

- C.48 To ensure that additions and amendments to the register of moveable assets are notified to Finance in accordance with arrangements defined by the CFO.

- C.49 To ensure that assets are identified, their location recorded and that they are appropriately marked and insured.

- C.50 To consult the CFO in any case where security is thought to be defective or where it is considered that special security arrangements may be needed.

- C.51 To ensure cash holdings on premises are kept to a minimum.

- C.52 To ensure that keys to safes and similar receptacles are carried on the person of those responsible at all times; loss of any such keys must be reported to the CFO as soon as possible.

- C.53 To record all disposal or part exchange of assets that should normally be by competitive tender or public auction, unless, following consultation with the CFO, the relevant Cabinet Member, Cabinet or Full Council (as appropriate) agrees otherwise.

- C.54 To arrange for the valuation of assets for accounting purposes to meet requirements specified by the CFO.

- C.55 To ensure that all employees are aware that they have a personal responsibility with regard to the protection and confidentiality of information, whether held in manual or

computerised records. Information may be sensitive or privileged, or may possess some intrinsic value, and its disclosure or loss could result in a cost to the authority in some way. - C.56 To maintain inventories and record an adequate description of furniture, fittings, equipment, plant and machinery above £200 in value.

- C.57 To carry out an annual check of all items on the inventory in order to verify location, review, condition and to take action in relation to surpluses or deficiencies, annotating the inventory accordingly. Attractive and portable items such as computers, cameras and video recorders should be identified with security markings as belonging to the authority.

- C.58 To make sure that property is only used in the course of the authority’s business, unless the Chief Officer concerned has given permission otherwise.

- C.59 To make arrangements for the care and custody of stocks and stores in the department.

- C.60 To ensure stocks are maintained at reasonable levels and are subject to a regular independent physical check. All discrepancies should be investigated and pursued to a

satisfactory conclusion. - C.61 To investigate and remove from the authority’s records (i.e. write off) discrepancies as necessary, or to obtain Cabinet approval if they are in excess of a predetermined limit.

- C.62 To authorise or write off disposal of redundant stocks and equipment. Procedures for disposal of such stocks and equipment should be by competitive quotations or auction, unless, following consultation with the CFO, Cabinet decides otherwise in a particular case.

- C.63 To seek Cabinet approval to the write-off of redundant stocks and equipment in excess of a predetermined sum.

- C.64 To ensure that, in the event of any disaster, contingency plans for the security of assets and continuity of service or system failure are in place.

Asets – Disposal

Responsibilities of the CFO

- C.65 To issue guidelines representing best practice for disposal of assets. Corporate Property Standards should be followed for disposals of Land and Buildings.

- C.66 To ensure appropriate accounting entries are made to remove the value of disposed assets from the authority’s records and to include the sale proceeds if appropriate.

Responsibilities of Chief Officers

- C.67 To dispose of surplus or obsolete materials, stores or equipment in accordance with the guidelines issued by the CFO.

- C.68 To ensure that income received for the disposal of an asset is properly banked and coded

Treasury Management

All financial transactions actioned as part of the Council’s Treasury Management function will be undertaken in line with the approved Treasury Management Strategy and practices but will fall outside of the Delegated Decision Notice process.

Responsibilities of CFO

- C.69 To arrange the borrowing and investments of the authority in such a manner as to comply with the CIPFA Code of Practice on Treasury Management and the authority’s treasury management policy statement and strategy.

- C.70 To report a proposed treasury management strategy for the coming financial year to Full Council at, or before the start of, each financial year.

- C.71 To report to Full Council not less than twice in each financial year on the activities of the treasury management operation and on the exercise of his or her delegated treasury management powers. One such report will comprise an annual report on treasury management for presentation by 30 September of the succeeding financial year.

- C.72 To operate bank accounts as are considered necessary – opening or closing any bank account shall require the approval of the CFO.

- C.73 To ensure that all investments of money are made in the name of the authority or in the name of nominees approved by Full Council.

- C.74 To ensure that all securities that are the property of the authority or its nominees and the title deeds of all property in the authority’s ownership are held in the custody of the appropriate Chief Officer.

- C.75 To affect all borrowings in the name of the authority.

- C.76 To act as the authority’s registrar of stocks, bonds and mortgages and to maintain records of all borrowing of money by the authority.

Responsibilities of Chief Officers

- C.77 To ensure that loans are not made to third parties and that interests are not acquired in companies, joint ventures or other enterprises without the approval, following consultation with the CFO, of Full Council or Cabinet as appropriate, subject to the criterion as detailed in E.9.

- C.78 To arrange for all trust funds to be held, wherever possible, in the name of the authority. All Officers acting as trustees by virtue of their official position shall deposit securities, etc relating to the trust with CFO, unless the deed otherwise provides.

- C.79 To arrange, where funds are held on behalf of third parties, for their secure administration, approved by the CFO, and to maintain written records of all transactions.

- C.80 To ensure that trust funds are operated within any relevant legislation and the specific requirements for each trust.

- C.81 To follow the instructions on banking issued by the CFO.

D: Systems and Procedures

General

Responsibilities of the CFO

- D.1 To make arrangements for the proper administration of the authority’s financial affairs, including to:

- a. Issue advice, guidance and procedures for Officers and others acting on the authority’s behalf

- b. Determine the accounting systems, form of accounts and supporting financial records

- c. Establish arrangements for audit of the authority’s financial affairs

- d. Approve any new financial systems to be introduced

- e. Approve any changes to be made to existing financial systems

Responsibilities of Chief Officers

- D.2 To ensure that accounting records are properly maintained and held securely.

- D.3 To ensure that vouchers and documents with financial implications are not destroyed, except in accordance with arrangements approved by the CFO.

- D.4 To ensure that a complete management trail, allowing financial transactions to be traced from the accounting records to the original document, and vice versa, is maintained.

- D.5 To incorporate appropriate controls to ensure that, where relevant:

- a. All input is genuine, complete, accurate, timely and not previously processed

- b. All processing is carried out in an accurate, complete and timely manner

- c. Output from the system is complete, accurate and timely

- D.6 To ensure that the organisational structure provides an appropriate segregation of duties, an adequate level of internal control, and that the risk of fraud or other malpractice is minimised.

- D.7 To ensure there is a documented and tested disaster recovery plan to allow information system processing to resume quickly in the event of an interruption.

- D.8 To ensure that systems are documented and staff trained in operations.

- D.9 To consult with the CFO before changing any existing system or introducing new systems.

- D.10 To establish a scheme of delegation identifying Officers authorised to act upon the Chief Officer’s behalf, or on behalf of Cabinet, in respect of payments, income collection and placing orders, including variations, and showing the limits of their authority.

- D.11 Where relevant, to supply lists of authorised Officers, with specimen signatures if required, and delegated limits, to the CFO, together with any subsequent variations.

- D.12 To ensure that effective contingency arrangements, including back-up procedures for computer systems are in place. Wherever possible, back-up information should be

securely retained in a fireproof location, preferably off site or at an alternative location within the building. - D.13 To ensure that, where appropriate, computer systems are registered in accordance with data protection legislation and that staff are aware of their responsibilities under the legislation.

- D.14 To ensure that the authority's IT Standards issued by the appropriate Head of Service are observed, and that in particular all computerised data, computer equipment and software are protected from loss and damage through theft, vandalism, etc.

- D.15 To comply with the copyright, designs and patents legislation and, in particular, to ensure that:

- a. Only software legally acquired and installed by the authority is used on its computers

- b. Staff are aware of legislative provisions

- c. In developing systems, due regard is given to the issue of intellectual property rights

Income

Responsibilities of the CFO

- D.16 To agree arrangements for the collection of all income due to the authority, and to approve the procedures, systems and documentation for its collection.

- D.17 To provide advice to Chief Officers on the statutory regulations which relate to the collection and accounting of income.

- D.18 To assess and approve the form of receipts used.

- D.19 To undertake weekly reconciliations of all deposits to the authority’s bank accounts.

- D.20 To provide an accounting system which records income and provides relevant information to Chief Officers so that income can be monitored.

- D.21 To maintain a Value Added Tax (VAT) account and supply HM Revenues & Customs (HMRC) with such details, explanations and statutory returns as required.

- D.22 To provide a system for the collection and control of credit income, and of sundry debts.

- D.23 To create, monitor and maintain a provision for bad and doubtful debts.

- D.24 To annually review the policy for writing off debts and the terms of credit. Cabinet is responsible for approving the procedures for writing off debts as part of the overall control framework of accountability and control.

- D.25 To approve all debts to be written off up to the value of £200,000 and to keep a record of all sums written off up to the approved limit. Once raised, no bona fide debt may be cancelled, except by full payment or by its formal writing off. A credit note to replace a debt can only be issued to correct a factual inaccuracy or administrative error in the calculation and/or billing of the original debt.

- D.26 To obtain the approval of Cabinet when writing off debts in excess of £200,000.

Responsibilities of Chief Officers

- D.27 To establish proposals for a charging policy for the supply of goods or services, including the appropriate charging of VAT, and to review it regularly, in line with corporate policies.

- D.28 To separate the responsibility for identifying amounts due and the responsibility for collection, as far as is practicable.

- D.29 To establish and initiate appropriate recovery procedures, including legal action where necessary, for debts that are not paid promptly.

- D.30 To issue official receipts or to maintain other documentation for income

- D.31 To ensure that at least two employees are present when post is opened so that money received by post is properly identified and recorded.

- D.32 To hold securely receipts, tickets and other records of income for the appropriate period.

- D.33 To lock away all income to safeguard against loss or theft, and to ensure the security of cash handling.

- D.34 To ensure that income is paid fully and promptly into the appropriate authority bank account in the form in which it is received. Appropriate details should be recorded on to paying-in slips to provide an audit trail. Money collected and deposited must be reconciled to the bank account and the ledger system on a regular basis appropriate to the level of transactions

- D.35 To ensure income is not used to cash personal cheques or other payments.

- D.36 To supply the CFO with details relating to work done, goods supplied, services rendered or other amounts due, to enable the CFO to record correctly the sums due to the authority and to ensure accounts are sent out promptly. To do this, Chief Officers should use established performance management systems to monitor recovery of income and flag up areas of concern to the CFO. Chief Officers have a responsibility to assist the CFO in collecting debts that they have originated, by providing any further information requested by the debtor, and in pursuing the matter on the authority’s behalf. Only up to approved levels of cash can be held on the premises.

- D.37 To keep a record of any transfer of money between employees. The receiving Officer must sign for the transfer and the transferor must retain a copy.

- D.38 To notify the CFO of outstanding income relating to the previous financial year as soon as possible after 31 March in line with the timetable determined by the CFO.

Ordering and Paying for Work, Goods and Services

Responsibilities of the CFO

- D.39 To ensure that all the authority’s financial systems and procedures are sound and properly administered.

- D.40 To ensure that a budgetary control system is established that enables commitments incurred by placing orders to be shown against the appropriate budget allocation so that they can be taken into account in budget monitoring reports.

- D.41 To approve any changes to existing financial systems and to approve any new systems before they are introduced.

- D.42 To approve the form of official orders and associated terms and conditions.

- D.43 To make payments from the authority’s funds on the Chief Officer’s authorisation that the expenditure has been duly incurred in accordance with financial regulations.

- D.44 To make payments, whether or not provision exists within the estimates, where the payment is specifically required by statute or is made under a court order.

- D.45 To make payments to contractors on the certificate of the appropriate Chief Officer, which must include details of the value of work, retention money, amounts previously certified and amounts now certified.

- D.46 To provide advice and encouragement on making payments by the most economical means.

- D.47 To provide, as necessary, cash change floats, and approve and set up bank imprest accounts to meet minor expenditure on behalf of the authority and to prescribe rules for operating these accounts.

- D.48 To maintain a record of all such cash floats and bank imprest accounts, and periodically to review the arrangements for the safe custody and control of them.

- D.49 To hold a central record of the scheme of delegation identifying Officers authorised to approve payments, orders and variations up to the value of £2 million as agreed by the Executive Director for each service.

- D.50 Payments, orders and variations over £2 million must be approved by the Executive Director in consultation with the CFO and Cabinet Member for the service.

Responsibilities of Chief Officers

- D.51 To ensure that unique numbered official orders are used for all goods and services, wherever possible in accordance with the Council’s No Purchase Order No Pay policy.

- D.52 To ensure official orders are not used to obtain goods or services for private use.

- D.53 To ensure that only those designated staff initiate or authorise orders and to maintain an up-to-date list of such designated staff, identifying authorisation limits. The authoriser of the order should be satisfied that the goods and services ordered are appropriate and needed, that there is adequate budgetary provision and that quotations or tenders have been obtained if necessary. Best value principles should underpin the authority’s approach to procurement and the Contract Procedure Rules must be adhered to when procuring on behalf of the Council. Value for money should always be achieved.

- D.54 To ensure that goods and services are checked on receipt to verify that they are in accordance with the order. Where possible a different Officer from the person who authorised the order should always carry out this check. If appropriate, entries should then be made in inventories or stores records.

- D.55 To ensure that payment is not made unless a proper VAT invoice has been received, checked, coded and certified for payment, confirming that:

- a. The goods or services have been received

- b. The invoice has not previously been paid

- c. The expenditure has been properly incurred and is within budget provision

- d. Prices and arithmetic are correct and accord with quotations, tenders, contracts or catalogue prices

- e. Tax has been correctly accounted for(f) The invoice is correctly coded

- f. Discounts have been taken where available

- g. Appropriate entries will be made in accounting records

- D.56 For the avoidance of doubt, no pre-payment for goods, services or suppliers shall beallowed above the value of £15,000, without the prior written consent of the CFO and the Director of Legal & Business Services.

- D.57 To ensure no Officer authorises a payment to her or himself, and where practical no Officer should authorise an invoice for which the Officer raised the order.

- D.58 To ensure controls are regularly reviewed to verify they are in place and adequate for the efficient management of the system, which enables invoices to be examined, verified and authorised as properly payable

- D.59 To ensure that payments are not made on a photocopied or faxed invoice, statement or other document other than the formal invoice. Any instances of these being rendered should be reported to the Chief Internal Auditor unless a written explanation giving the reason is attached. Any copy invoice must be clearly marked by the supplier that it is a copy.

- D.60 To encourage suppliers of goods and services to receive payment by the most economical means for the authority. It is essential, however, that payments made by direct debit have the prior approval of the CFO.

- D.61 To ensure that the Council obtains best value from purchases by taking appropriate steps to obtain competitive prices for goods and services of the appropriate quality, with regard to the authority's Contract Procedure Rules.

- D.62 To utilise any established central purchasing procedures in putting purchases, where appropriate, out to competitive quotation or tender. These will comply with the authority's Contract Procedure Rules.

- D.63 To ensure that employees are aware of the national code of conduct for local government employees (summarised in the procedures and conditions of employment manual).

- D.64 To ensure that loans, leasing or rental arrangements are not entered into without prior agreement from the CFO. This is because of the potential impact on the authority’s

borrowing powers, to protect the authority against entering into unapproved credit arrangements and to ensure that value for money is being obtained. - D.65 To notify the CFO of outstanding expenditure relating to the previous financial year as soon as possible after 31 March in line with the timetable determined by the CFO.

- D.66 With regard to contracts for construction and alterations to buildings and for civil engineering works, to document and agree with the CFO, the systems and procedures to be adopted in relation to financial aspects, including:

- a. Certification of interim and final payments

- b. Checking, recording and authorising payments

- c. Monitoring and controlling capital schemes

- d. Validation of subcontractors’ tax status

- D.67 To notify the CFO immediately of any expenditure to be incurred as a result of statute/court order where there is no budgetary provision.

- D.68 To ensure that all appropriate payment records are retained and stored for the defined period, in accordance with the document retention schedule

- D.69 To ensure that employees operating an imprest account:

- a. Obtain and retain vouchers to support each payment from the imprest account, including where appropriate an official receipted VAT invoice

- b. Make adequate arrangements for the safe custody of the account

- c. Produce upon demand by the CFO cash and all vouchers to the total value of the imprest amount

- d. Record transactions promptly

- e. Reconcile and balance the account at least monthly; reconciliation sheets to be signed and retained by the imprest holder

- f. Provide the CFO with a certificate of the value of the account held at the end of Period 11 each year, detailing the breakdown between cash at bank, cash in hand, petty cash floats advanced and vouchers.

- g. Ensure that the float is never used to cash personal cheques or to make personal loans and that the only payments into the account are the reimbursement of the float and change relating to purchases where an advance has been made

- h. On leaving the authority’s employment or otherwise ceasing to be entitled to hold an imprest advance, an employee shall account to the CFO for the amount advanced to him or her.

- i. Follow the Council’s Petty Cash policy.

Payments to Employees and Members

Responsibilities of the CFO

- D.70 To arrange and control secure and reliable payment of salaries, wages, compensation or other emoluments to existing and former employees, in accordance with procedures prescribed by him or her, on the due date.

- D.71 To record and make arrangements for the accurate and timely payment of tax, superannuation and other deductions.

- D.72 To make arrangements for payment of all travel and subsistence claims or financial loss allowance.

- D.73 To make arrangements for paying Members travel or other allowances.

- D.74 To provide advice and encouragement to Members, Chief Officers and employees in order to secure payment of allowances, salaries and wages by the most economical means.

- D.75 To ensure that there are adequate arrangements for administering superannuation matters on a day-to-day basis.

- D.76 To act as an advisor to Chief Officers on areas such as national insurance and pension contributions, as appropriate.

Responsibilities of Chief Officers

- D.77 To ensure appointments are made in accordance with the regulations of the authority and approved establishments, grades and scale of pay and that adequate budget provision is available.

- D.78 To notify the CFO of all appointments, terminations or variations which may affect the pay or pension of an employee or former employee, in the form and to the timescale required by the CFO.

- D.79 To ensure that adequate and effective systems and procedures are operated, so that:

- a. Payments are only authorised to bona fide employees

- b. Payments are only made where there is a valid entitlement

- c. Conditions and contracts of employment are correctly applied

- d. Employees’ names listed on the payroll are checked at regular intervals to verify accuracy and completeness

- D.80 To ensure that only those staff designated by them initiate or authorise payroll documentation and to maintain a list of such designated staff, including where appropriate specimen signatures identifying in each case the limits of their authority.

- D.81 To ensure that payroll transactions are processed only through the payroll system. Chief Officers should give careful consideration to the employment status of individuals employed on a self-employed consultant or subcontract basis. HMRC applies a tigh definition for employee status, and in cases of doubt, advice should be sought from the CFO.

- D.82 To certify travel and subsistence claims and other allowances. Certification is taken to mean that journeys were authorised and expenses properly and necessarily incurred, and that allowances are properly payable by the authority, ensuring that cost-effective use of travel arrangements is achieved. Due consideration should be given to tax implications and that the CFO is informed where appropriate.

- D.83 To ensure that the CFO is notified of the details of any employee benefits in kind, to enable full and complete reporting within the income tax self-assessment system.

- D.84 To ensure that all appropriate payroll documents are retained and stored for the defined period in accordance with the document retention schedule. Responsibilities of Members

- D.85 To submit claims for Members’ travel and subsistence allowances on a monthly basis and, in any event, within one month of the year end

Taxation

Responsibilities of the CFO

- D.86 To complete all HMRC returns regarding PAYE.

- D.87 To complete a monthly return of VAT inputs and outputs to HMRC.

- D.88 To provide details to HMRC regarding the construction industry tax deduction scheme.

- D.89 To complete all relevant company returns.

- D.90 To complete corporation returns for wholly owned companies.

- D.91 To advise Chief Officers, in the light of guidance issued by appropriate bodies and relevant legislation as it applies, on all taxation issues that affect the authority, and to maintain up-to-date guidance for all authority employees on taxation issues.

Responsibilities of Chief Officers

- D.92 To ensure that the correct VAT liability is attached to all income due and that all VAT recoverable on purchases complies with HMRC regulations.

- D.93 To ensure that, where construction and maintenance works are undertaken, the contractor fulfils the necessary construction industry tax deduction requirements.

- D.94 To ensure that all persons employed by the authority are added to the authority’s payroll and tax deducted from any payments. The IR35 guidance should be followed for all offpayroll workers who will be subject to PAYE deductions unless a determination has been issued by the IR35 team stating otherwise. As per the Consultants Policy a business case must be submitted for approval to Executive Management Board before engaging consultants.

- D.95 To follow the guidance on taxation issued by the CFO, including the Tax Evasion Policy.

Quasi Commercial operations

Responsibilities of the CFO

- D.96 To advise on the establishment and operation of trading accounts and business units.

Responsibilities of Chief Officers

- D.97 To consult with the CFO where a business unit wishes to enter into a contract with a third party where the contract expiry date exceeds the remaining life of their main contract with the authority. In general, such contracts should not be entered into unless they can be terminated within the main contract period without penalty.

- D.98 To observe all statutory requirements in relation to business units, including the maintenance of a separate revenue account to which all relevant income is credited and all relevant expenditure, including overhead costs, is charged, and to produce an annual report in support of the final accounts.

- D.99 To ensure that the same accounting principles are applied in relation to trading accounts as for other services or business units.

- D.100 To ensure that each business unit prepares an annual business plan in accordance with published guidelines.

E: External Arrangements

Partnerships

Responsibilities of the CFO

- E.1 To advise on effective controls that will ensure that resources are not wasted.

- E.2 To advise on the key elements of funding a project including:

- a. A scheme appraisal for financial viability in both the current and future years

- b. Risk appraisal and management

- c. Resourcing, including taxation issues

- d. Audit, security and control requirements

- e. Carry-forward arrangements.

- E.3 To ensure that the accounting arrangements are satisfactory.

Responsibilities of Chief Officers

- E.4 To maintain a register of all contracts entered into with external bodies in accordance with procedures specified by the CFO.

- E.5 To ensure that, before entering into agreements with external bodies, appropriate approvals have been obtained and a risk management appraisal has been prepared for the CFO.

- E.6 To ensure that such agreements and arrangements do not impact adversely upon the services provided by the authority.

- E.7 To ensure that all agreements and arrangements are properly documented.